Affordability assessments for mortgages and small business loans are notoriously lengthy, taking up an unnecessary amount of time for both borrower and lender. FriendlyScore, a London-based FinTech, is employing open banking technology to help lenders dramatically streamline this process.

The Problem with Affordability Assessments.

Anyone who has been through the application process for a mortgage or small business loan knows the routine: protracted application forms, multiple in-person meetings, sourcing verification documents, estimating spending habits, double checks, amendments, lengthy processing times..

And if you’re unlucky, after all of that… rejection.

Many of the inconveniences mentioned above stem from what is known as an affordability assessment, a process deployed by lenders to determine a borrower’s capacity to repay the loan or mortgage. Unfortunately, affordability assessments are unavoidably lengthy; data concerning spending habits, income, credit obligations, etc. has to be gathered and verified in order that the lender can make a genuine appraisal. So if we can’t shorten the assessment itself, what can be done to speed the process up?

An Affordability Tool for the Open Banking Era

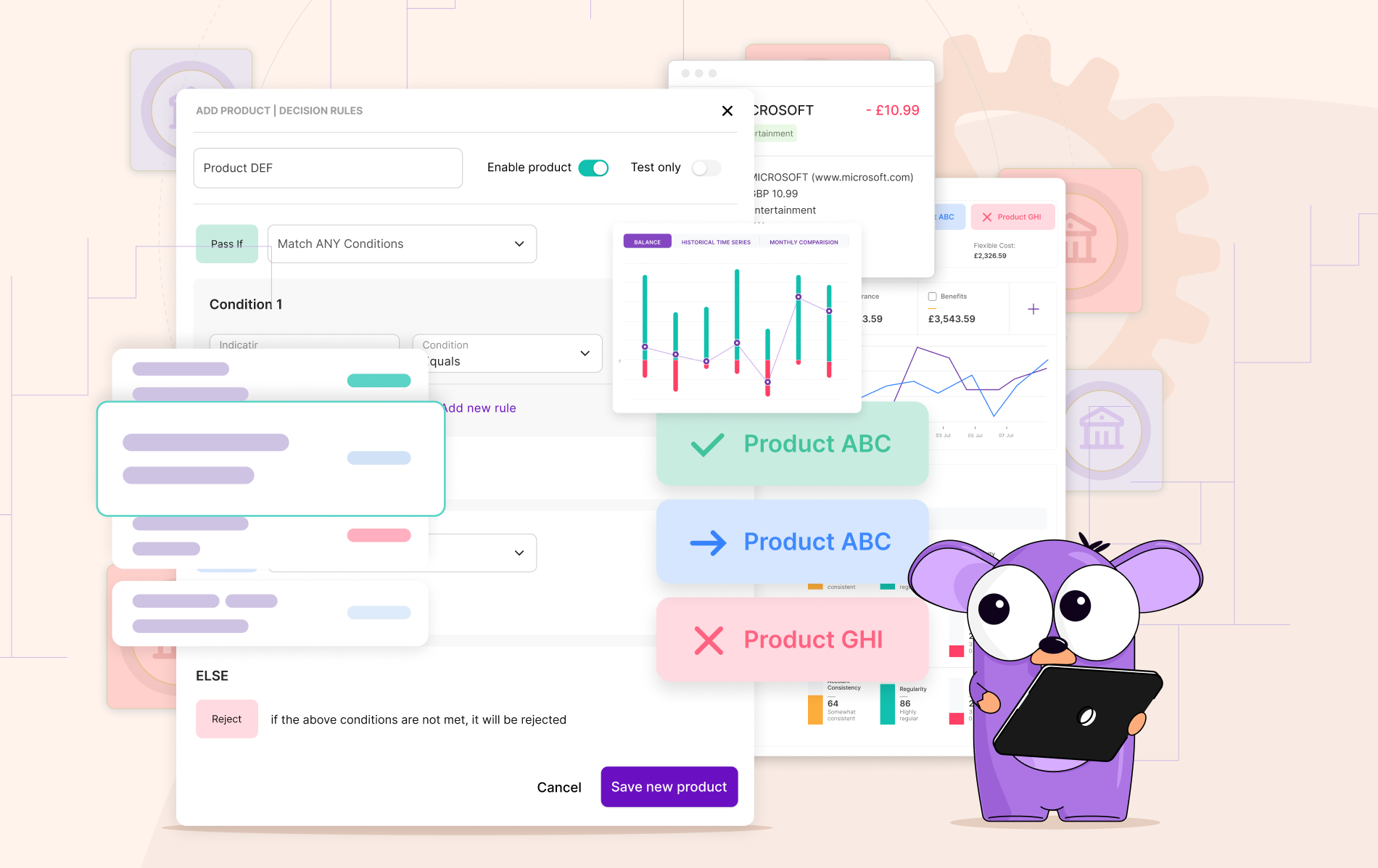

Here is where a company like FriendlyScore is able to help. By extracting transaction data from a borrower’s bank account via open banking, FriendlyScore is able to pre-populate many of the fields commonly found in a loan or mortgage affordability assessment. Borrowers can skip manually filling in forms and trying to estimate their average monthly grocery bill because all of this is quantified instantly and with complete precision through open banking. And it’s not only your income and spending habits which can be automatically filled either: employment details, credit obligations and problematic financial behaviours such as gambling can all be inferred through transaction data. What’s more, there is no need for supporting documents to verify any of this data, as it is all extracted directly from the borrower’s bank account!

So whilst this reduces the need for things like manual form-filling and sourcing verification documents, what about the lengthy decision times, multiple meetings with the bank and, most of all, those annoying rejections?

FriendlyScore again has the answer with its Affordability Score, a statistical algorithm which identifies patterns within the borrower’s financial data to produce a probabilistic measure of their capacity to repay the loan. The lender can then use this score as a basis for screening eligibility from the outset, pre-approving customers for certain products, or adjusting the terms of products for which a customer has already applied. This largely eliminates the back and forth between lender and borrower, ensures the customer is suitably matched to their product, and minimises the chance of rejection further down the line.

By offering this more streamlined version of the traditional affordability assessment, lenders can improve the overall experience for their customers during what can often be a stressful time.

FriendlyScore is a London-based FinTech offering open banking-based solutions for affordability assessment to lenders. Find out more by visiting our website at www.friendlyscore.com today.