29 May 2025

The AI Advantage: How Smart Data is Redefining Affordability Assessments

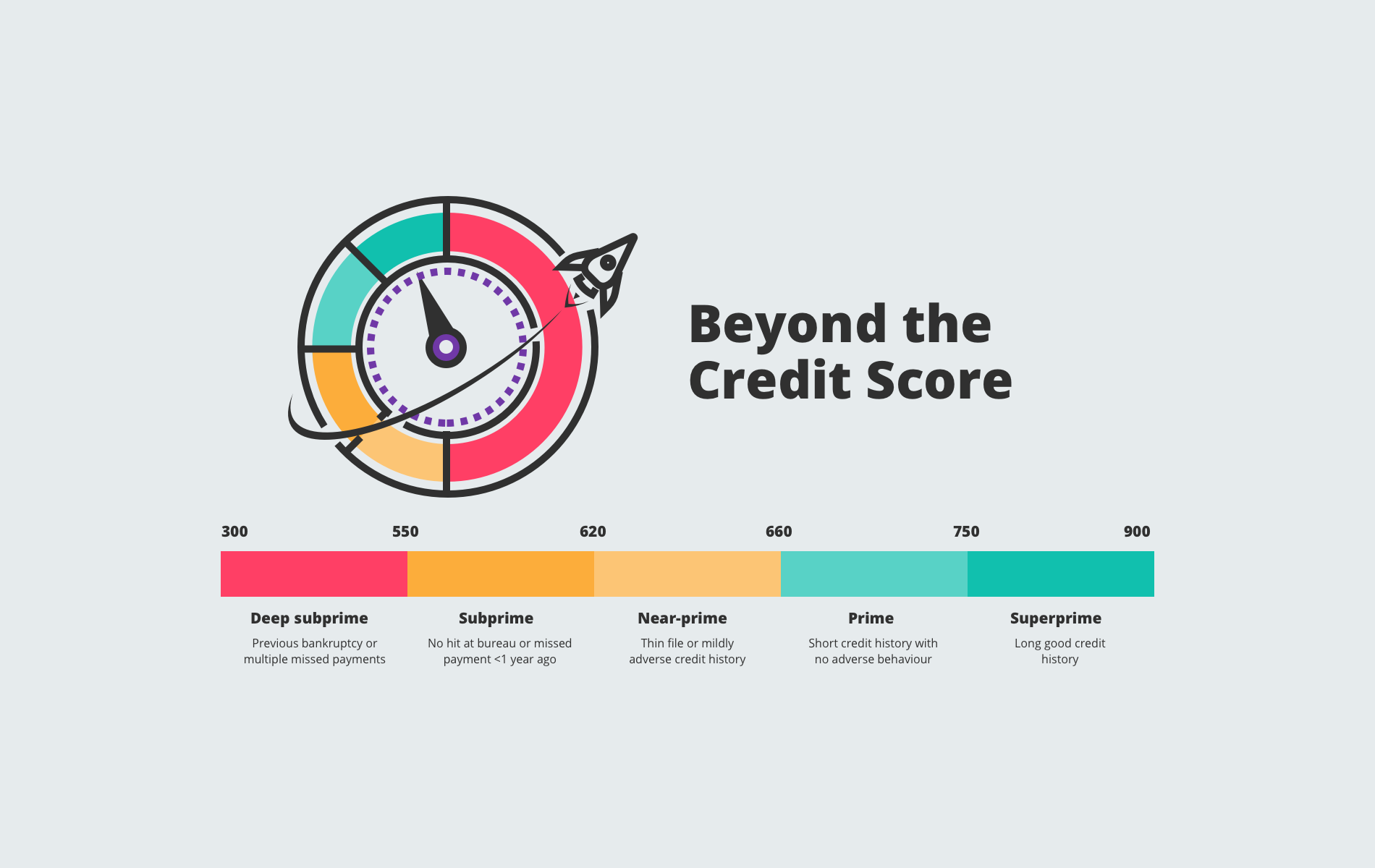

In a time where accuracy and efficiency are paramount, the need for innovative affordability assessments has never been greater. Traditional methods are quickly being replaced by AI-powered, data-driven solutions that offer real-time insights, enabling more accurate and efficient decision-making. AI is transforming how organizations assess affordability, streamlining processes to be faster, more reliable, and better suited to today’s rapidly changing landscape.