As the UK’s COVID-19 lockdown enters its second month, and with no clear end in sight, small businesses are bearing an increasingly high financial burden. The government has responded in the form of their £330bn Coronavirus Business Interruption Loan Scheme (CBILS), but to date only £2.8bn of this has actually been disbursed. With current estimates predicting that one-fifth of all UK SMEs will close or fail by the end of June, time is of the essence.

What’s the holdup?

An initial group of around 40 lenders, which included major players such as the CMA9, were accredited by the British Business Bank (BBB) to dispense relief loans. However, money has been slow to get out of the door. Whilst the government scheme provides an 80% guarantee against the outstanding balance, banks take on the remainder of the risk and therefore still must adhere to established and often lengthy credit risk protocols. Factor in the reduced working capacity, and it’s easy to see why borrowers are being frustrated.

In recent weeks, fintech lenders, including challenger banks and digital lending platforms, have been lobbying, with some success, for BBB accreditation. Whilst these smaller organisations are more agile and better suited for quick loan turnarounds, many do not have the capability to properly assess business creditworthiness and are likewise exposed to the residual credit risk.

The test for banks, challengers and digital lenders then is to be agile whilst properly managing credit risk. Agility translates to fast application and approval processes, whilst proper credit risk mangement calls for a robust assessment of business creditworthiness. An open banking fintech app, positioned between business and lender, can provide such functionality.

FriendlyScore

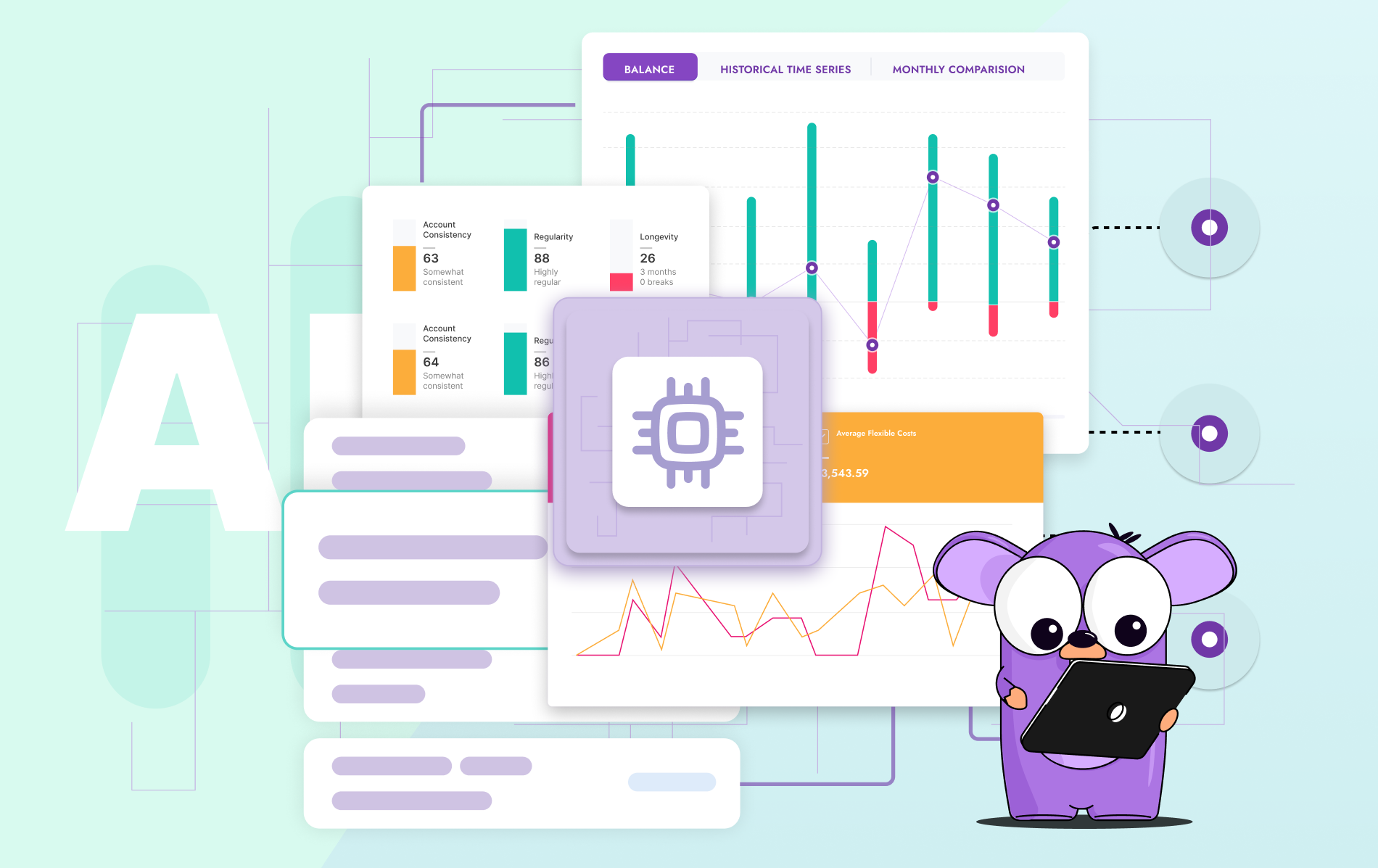

FriendlyScore is an off the shelf analytics software solution which leverages open banking to both streamline the loan application process and comprehensively assess SME creditworthiness. It works as follows: the prospective borrower visits the lender’s app or website and is asked to connect their business account via the white labelled FriendlyScore application. Upon doing this, the software near-instantaneously extracts, processes and analyses the transaction data associated with this account and displays the results to the lender via a user-friendly dashboard. Inside the dashboard, the lender can access loan application data such as:

- Cash flow analysis, including historical income and expenditure data, broken down by transaction category

- KYC information, such as company name, address and legal structure

- Payroll details, including payment dates, frequency and expected amount

Also included within the dashboard is a comprehensive assessment of business creditworthiness, which includes:

- Financial credibility score, which quantifies the likelihood a borrower will default on credit

- Affordability score, which measures the solvency of a business and it’s near-term capacity to repay credit

- Performance indicators, such as profitability and debt ratios, missed repayments and recent credit products

With such features on offer, FriendlyScore represents a silent but incredibly powerful tool which enables lenders to quickly get money into the hands of business owners at this crucial time, whilst being confident that any residual credit risk is mitigated.

FriendlyScore is currently looking to partner with lenders participating in the CBILS to assist in getting loan relief to business owners. Find out more today by visiting www.friendlyscore.com.