The first step to getting your CU open banking-ready is to find a licensed third-party provider which facilitates this data sharing. The provider may also offer analytical packages which extract useful information from the data, delivering value to both business and customer. FriendlyScore is an FCA-licensed AISP (Account Information Services Provider) that brings the full range of open banking benefits to CUs.

So what are these benefits precisely?

Elimination of manual processes. Improved data quality. Faster credit decisions. And, ultimately, enhanced customer experience. With all of this on offer, it’s no surprise that credit unions are quickly embracing the open banking revolution.

But how are these benefits realised in practice? Say a CU receives a loan application, initiating the credit decision process. The underwriter needs to determine two things:

The credit riskof the customer (how likely they are to pay back the loan)

A customer’s affordability (how much they can afford to repay)

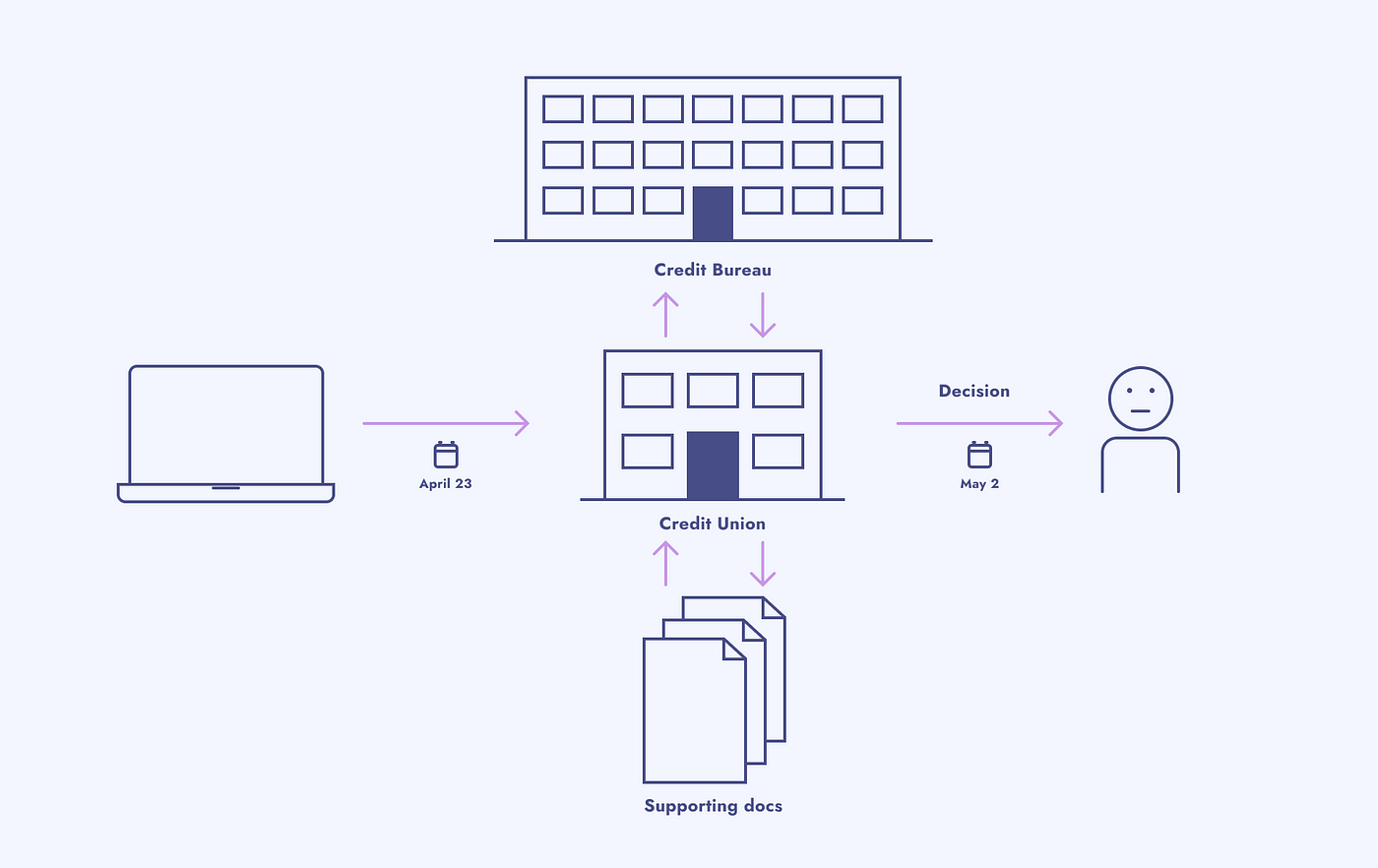

Underwriters will commonly perform a bureau search to determine credit risk. However, bureau data only concerns a customer’s use of credit products (such as credit cards). Useful data from other sources such as current accounts (think rent or utility payments) is missing from the decision. Further, bureau data is often weeks out of date, may be incomplete, and can take days to arrive.

On the other hand, assessing affordability requires that the underwriter find evidence of an applicant’s income and existing financial obligations. Sourcing of documents that can provide this information (such as bank statements and tenancy agreements) can also be a lengthy process and ultimately impact time-to-decision.

Above: The traditional loan application.

Once a customer fills in their initial application, the journey has only just begun. The credit union must perform checks with credit bureaus and source supporting documentation resulting in the customer waiting days before receiving a firm decision.

FriendlyScore: Bringing the power of open banking to CUs

FriendlyScore eliminates almost all of these nuisance factors associated with the traditional credit application process. Its software essentially acts as an interface between the customer and CU, enabling customers to share bank transaction data via open banking. FriendlyScore also performs the data processing necessary to deliver credit risk and affordability analytics directly to the underwriter. This process occurs near-instantly so the underwriter can be confident they are using the latest available data. Moreover, since this data is verified (customers are required to go through their bank’s secure verification process when sharing information), there is no need to source supporting documents for affordability checks.

FriendlyScore’s ability to eliminate these inefficiencies means CUs can make fast, accurate loan decisions and improve overall customer experience.

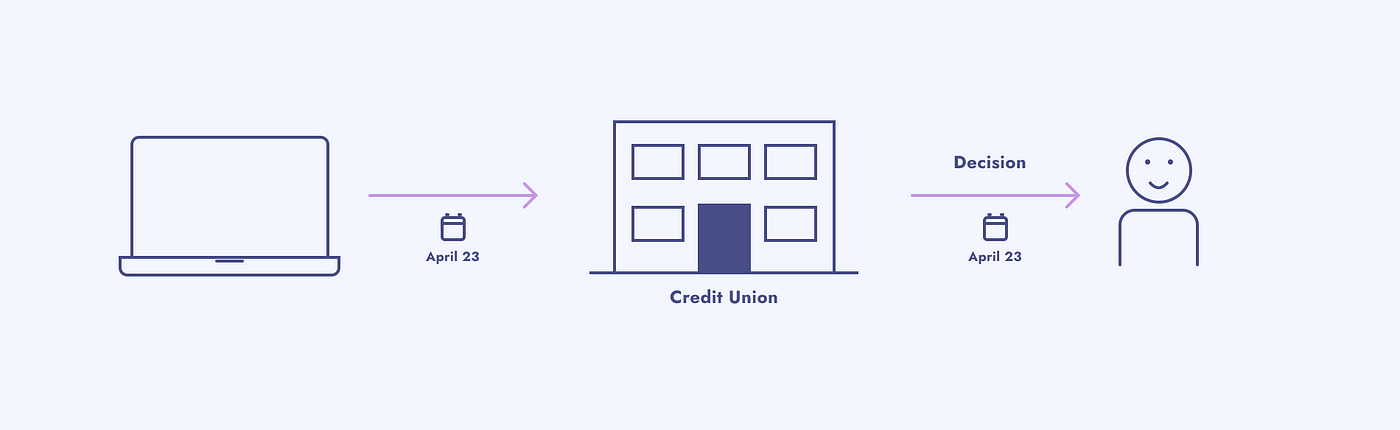

Above: The modern credit application, powered by FriendlyScore.

When a CU works with FriendlyScore, customers can begin sharing their banking data with the CU. Underwriters will also receive a host of credit risk and affordability analytics upon which to base a decision. By eliminating the need for bureau and verification checks, same-day loan decisions for customers can become the norm.

How can I get involved?

If moving to open banking-based technology is something your CU has been contemplating, there has never been a better time to get on board. And FriendlyScore makes this process quick and easy. Find out more today by visiting www.friendlyscore.com.

FriendlyScore is an Account Information Services Provider (AISP) licensed by the FCA. Our product delivers open banking connectivity and analytics to credit unions. We also offer free trials, so you can try us out before making any commitment to purchase.

In a time where accuracy and efficiency are paramount, the need for innovative affordability assessments has never been greater. Traditional methods are quickly being replaced by AI-powered, data-driven solutions that offer real-time insights, enabling more accurate and efficient decision-making. AI is transforming how organizations assess affordability, streamlining processes to be faster, more reliable, and better suited to today’s rapidly changing landscape.

Do you know that 2022 ended with over 2.4 million reports of fraud with losses reaching $8.8 billion? Financial transactions have been moving from paper-based to digital platforms which require more and more robust security protocols. Therefore, companies need more comprehensive fraud prevention and security protocols to make sure their online transactions are fully protected and error-free. One of the best tools designed to enhance your security protocols is Account Check.

A great advantage for a creditor company is the ability to categorize transactions into income and expense categories and fully automate the credit decisioning processes.