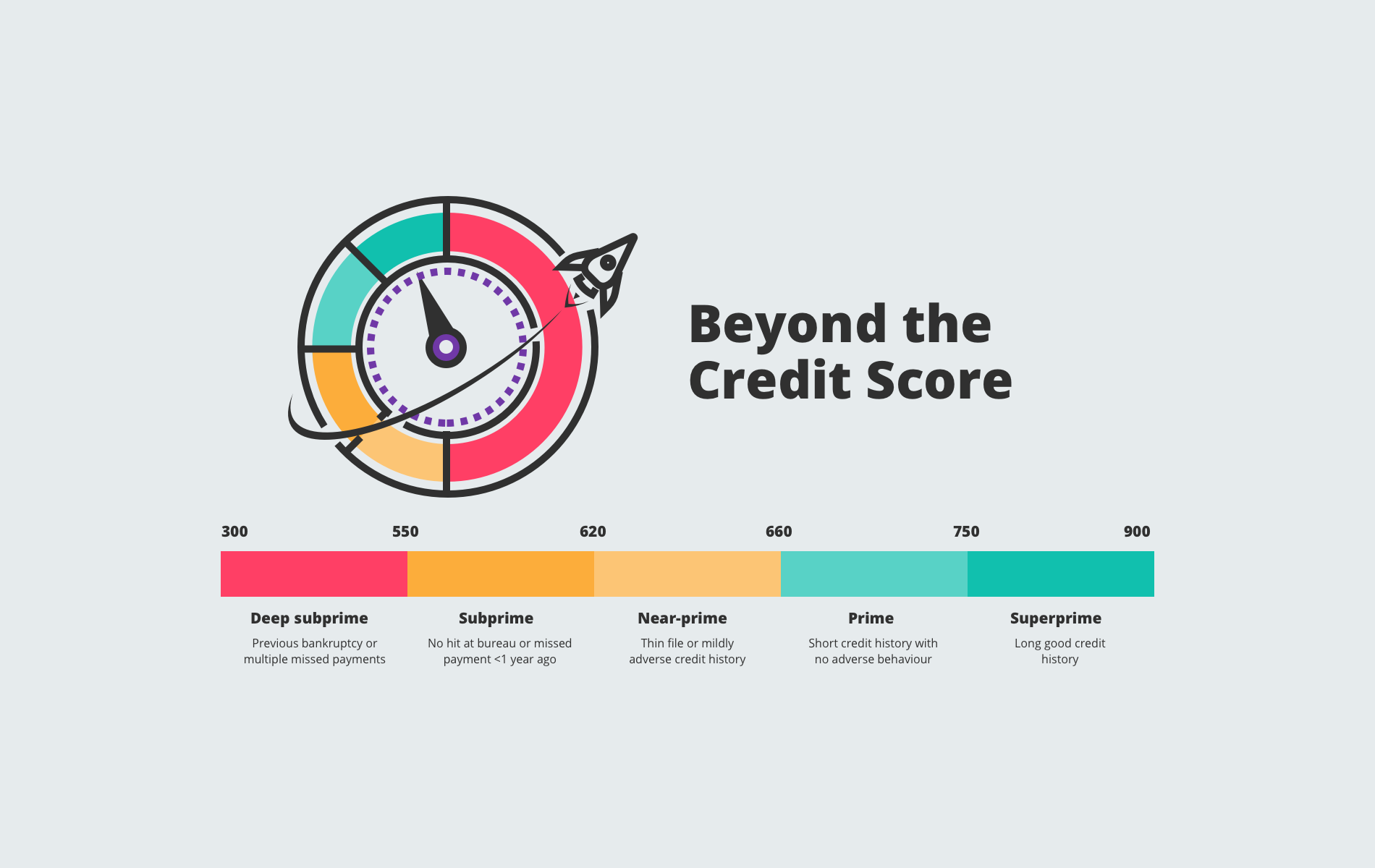

Credit scores have long been the benchmark for determining whether or not you are eligible for credit. Credit scores also determine the quality of credit you will receive: a higher score generally translates to lower interest rates. Whilst it is easy to determine the eligibility of individuals at either end of the scoring spectrum, there exists a subset of customers in the middle known as “near-prime” for which things are less clear.

Near-prime customers usually have a good credit history with a few mild blemishes (such as a missed payment over one year ago), or have a “thin file” at the credit bureau (i.e. a lack of history using credit products). Making up roughly one-quarter of the UK population, they tend to be susceptible to poor credit outcomes such as rejection and resorting to low quality credit such as high cost short term (payday) loans. However, it is estimated that around 10 to 20% of this group are actually perfectly creditworthy, representing something of an untapped market for credit providers. The question is, how to identify them?

Redefining Creditworthiness

Thin file customers are a direct consequence of the limitations of credit bureaus, which only collect data on an individual’s use of credit products, such as loans and credit cards. Activity on current or savings accounts does not factor into their calculation. Since approximately 97% of UK adults own some form of current account, the vast majority of thin-file customers would therefore stand to benefit from a credit assessment based on current account data.

Recognising the need for such an innovation, FriendlyScore have leveraged the power of Open Banking to model the creditworthiness of thin-file customers using transaction data from a user’s current account. A host of insights into credit eligibility can be extracted from this data, including:

- Spending patterns

- Employment information

- Income growth and trajectory

- Rent and utilities payments

- Savings contributions

Intuitively this approach makes sense: transactions such as rent and utility payments are similar in character to, say, a loan repayment. By connecting their bank data through FriendlyScore, thin file customers can now obtain a truly representative assessment of creditworthiness in seconds.

For other near-prime customers, the situation is slightly different. Information already exists at the credit bureau, yet some mildly adverse activity on their file is perhaps misrepresenting their true financial potential. For example, a customer may have missed a couple of credit card repayments over a year ago due to legitimate reasons, e.g. a large repair or medical expense.

FriendlyScore is able to consider several years’ worth of current account activity to contextualise adverse activity on an individual’s credit file, enabling lenders to successfully differentiate near-prime customers who are most likely to repay credit. Such insights can make the difference between an accept or a reject, or a prime or subprime rate of interest.

Summary

It is clear that assessments of creditworthiness need to evolve beyond the credit score in order to better serve thin filed and other near-prime customers. Using Open Banking, FriendlyScore can more accurately represent the creditworthiness of these customers, opening up the opportunity for lenders to expand their customer base and make fairer, more financially inclusive credit decisions.

FriendlyScore now offers Open Banking solutions which can help lenders better assess thin-file and other near prime customers. To find out more, visit www.friendlyscore.com today.