Recovering bad debt has always been a tough ask. Each stage of the process, from tracking down debtors to formulating suitable repayment agreements, has the potential to spiral into a laborious, time-consuming exercise. But some tasks commonly undertaken by collections agents now have the potential to be streamlined using Open Banking-based technologies, easing the burden for both agent and debtor.

FriendlyScore is now looking to implement such a use case within the industry, so here we take a look at some of the value it brings to the table.

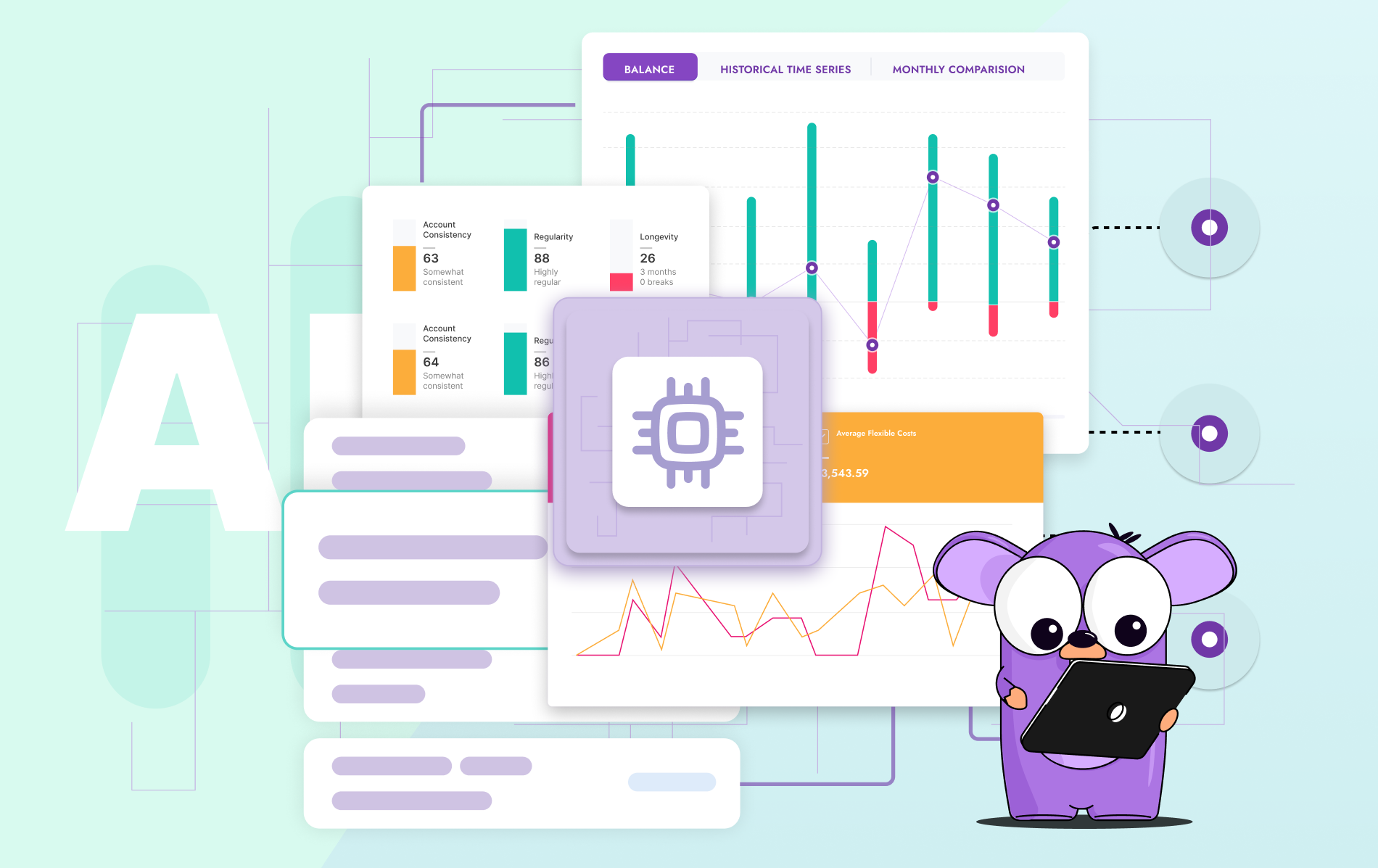

Obtaining accurate financial information

Gathering financial information on debtors almost universally involves some kind of income and expenditure statement. And whilst digital forms represent a step forward from the days of paper statements, self-certification remains fundamentally problematic. Incomplete, erroneous or misrepresented figures can delay agreements being made, or lead to repayment problems further down the line.

With FriendlyScore’s Open Banking solution, collections agents can now ask customers to connect their bank account(s) through a white-labelled app, whereupon accurate, verified income and expenditure information is extracted instantly. This data can then be viewed in a user-friendly dashboard or used to auto-populate standard income and expenditure statements, giving agents a firm basis on which to proceed.

Agreeing a repayment schedule

Negotiating repayment agreements is a delicate act, with the aim being to create a ‘win-win’ situation for both parties. A rigorous affordability assessment is key to success, and a common approach uses disposable income to figure out how much a debtor is able to repay. However this is often based on an individual’s financial circumstances at that time, rather than a more forward-looking analysis.

FriendlyScore offers an affordability measure using historical transaction data and time series analysis to measure the near-term likelihood of the debtor having insufficient funds to meet a certain repayment obligation. This is backed up by a series of “red-flag” markers such as gambling behaviour or ongoing missed repayments, which highlight any potential issues the agent may wish to address during the agreement process.

Ongoing monitoring of the agreement

Monitoring of repayment agreements currently involves agents checking in with the debtor at regular intervals, or chasing accounts which have relapsed into delinquency. But a more optimal solution could involve agents taking pre-emptive action based on signs of impending underperformance. Live Open Banking data gives agents the power to monitor income, expenditure, red-flag markers and affordability metrics in real time, and detect the early signs of delinquency.

Empowering Customers

One further possibility to optimise likelihood of repayment is to improve the financial capability of the debtor. Often even the smallest amount of help can have a huge impact, especially on those who are more financially vulnerable. FriendlyScore’s personal finance management toolkit enables collection agencies to provide users with key financial insights and a suite of complementary tools, such as budgeting planners and expense trackers, to help the debtor maintain good financial health.

FriendlyScore is currently offering Open Banking solutions for use in debt collection and recovery. If you are interested in exploring this opportunity further, please visit our website today at www.friendlyscore.com.