Open Banking recently celebrated its second birthday in the UK. Whilst it has received criticism from some quarters for being slow out of the blocks, it has now gathered more than one million active users, and an increasing number of innovative use cases coming from the FinTech sector could make 2020 the year that Open Banking finally cracks the mainstream.

Open Banking, hyped as the most fundamental shift in the financial services ecosystem in a generation, gives customers the power to authorise their bank to share transaction data with any other bank or authorised third-party provider they choose to use. This means customers can take advantage of a host of new financial services and smartphone applications which are now available in the market.

However, rather than setting the world alight as some expected, Open Banking’s progress has been more of a slow burn. This can be traced back to several factors, including a general lack of public awareness and slow implementation of the infrastructure to facilitate it. And whilst there was initially some scepticism surrounding the benefits of Open Banking, especially amongst the more established players in the market, it is now clear that collaborative efforts between all parties, from the biggest banks down to the smallest startups, can be of mutual benefit.

To elaborate upon this point, let us look at five interesting Open Banking use cases currently being offered by FriendlyScore which could help companies significantly streamline their workflows and get ahead of the curve in 2020.

Advanced personal finance management apps: Perhaps the most common type of Open Banking app available at present is the Personal Finance Manager (PFM). The most basic versions of these are account aggregators, however more advanced tools which offer features such as budgeting planners and financial coaching are now available. What’s more, these can be quickly integrated into existing company software, enabling banks and lenders to offer customers the resources to better manage credit repayments and improve their overall financial capability.

Alternative credit risk and affordability measures: Banks and lenders frequently miss out on the business of otherwise perfectly creditworthy individuals because of outdated credit scoring systems. But there is a simple solution: by taking into account a series of alternative credit risk predictors, such as spending behaviour, rent payments and employment details, all of which can be gleaned from Open Banking data, a more accurate and representative assessment of credit risk and affordability can be made than those based on internal or bureau data.

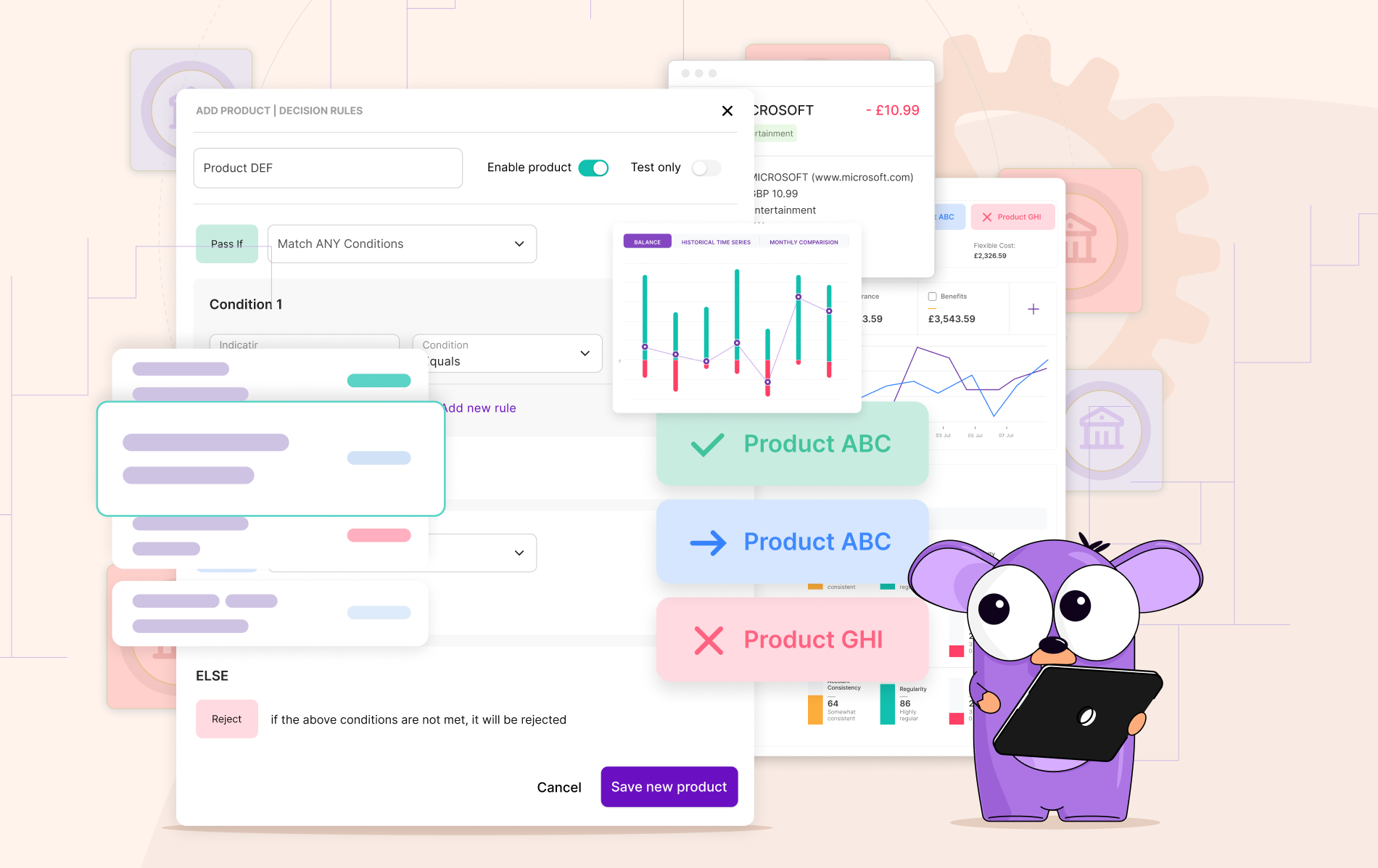

Automated credit applications: If you’ve ever applied for a mortgage or small business loan you know the drill: lengthy form-filling, sourcing documents, estimating figures - this can now all be bypassed using Open Banking. Customers can simply connect to their bank through a white-labelled app which extracts accurate data, processes it into a standard form and auto-populates their application. The result is improved decision times, a reduction in fraud or misrepresentation, and vastly enhanced CX.

Addressing vulnerable customers: The post-2008 regulatory landscape led to financial institutions taking conduct (or reputational) risk far more seriously. And in order to avoid past mistakes, and huge regulatory fines, treating customers fairly became a priority. One interesting use case employs data analytics to pinpoint financially vulnerable individuals using financial, behavioural and psychological traits isolated within Open Banking data. This solution can provide invaluable assistance for financial institutions in identifying and proactively managing conduct risk hazards within their credit book.

Collections and Recovery: For debt recovery companies, forming a successful collections strategy depends largely on how accurately metrics such as an individual’s income or spending habits can be quantified. Traditionally this has been done through a lengthy combination of interviews, form-filling and document sourcing; however, Open Banking offers a speedy alternative. The customer simply connects to the collections agency via a white-labelled app which instantly extracts these metrics, along with a range of further insights into cash flow patterns and customer behaviour.

Closing Thoughts

Open Banking is a necessity in our modern financial landscape, and the innovations which follow from it will set new standards with regards to what consumers expect from their financial service providers. This means collaborative efforts within the financial industry will be key in meeting the demands of a tech-hungry consumer market. And whilst Open Banking may have had something of a slow start to life, with innovative use cases from the FinTech sector increasing in number, scope and variety seemingly by the day, 2020 could be the year it finally catches a wave.

FriendlyScore offers a variety of Open Banking-based solutions for companies within the financial services sector and beyond. Find out how Open Banking can help improve your customers’ experience by visiting www.friendlyscore.com today.